Risk tolerance: What is it — and how can I measure it?

It’s more than just what feels right, say our experts, and it can change, depending on your goals. Here’s how to use it to help inform your investing decisions.

ALL INVESTING INVOLVES RISK. That’s one of the first things you’ll learn as you begin to invest to meet important goals, such as retirement and saving for college or buying a home. But just how much risk are you comfortable taking in order to pursue growth? To find that answer, it may help to understand a bit more about “risk” and “risk tolerance.”

“People tend to focus just on their comfort level with risk. But your ability to take risks, based on your financial situation, is just as important.”

—

senior quantitative analyst, Chief Investment Office, Merrill and Bank of America Private Bank

“When you invest, risk is the effect of uncertainty on progress toward your goals,” says Anil Suri, portfolio construction and investment analytics executive in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank. “While you hope for high returns, that hope needs to be balanced by the possibility of poor returns,” he adds. “Generally, the higher the risk, the greater your rewards — or losses — could be.”

That brings us to risk tolerance, officially defined by the U.S. Securities and Exchange Commission (SEC) as “an investor’s ability and willingness to lose some or all of an investment in exchange for greater potential returns.”1

“When assessing your personal risk tolerance, both sides of that equation, willingness and ability, need to work in tandem,” says Nevenka Vrdoljak, senior quantitative analyst with the CIO. “People tend to focus just on willingness — their comfort level with risk. But your ability to take risks, based on your personal financial situation, is just as important.”

Let’s look at both:

Your willingness to take risks

Whether the subject is money or mountain climbing, everyone’s comfort with risk differs. You’ve probably seen investment questionnaires that help you determine where you fall on the investing spectrum, from conservative (risk averse) to aggressive (willing to take on substantial investment risk). Your willingness is a part of who you are and tends not to change, even when your financial position does, Vrdoljak notes, and it should be an important consideration as you make your investment decisions.

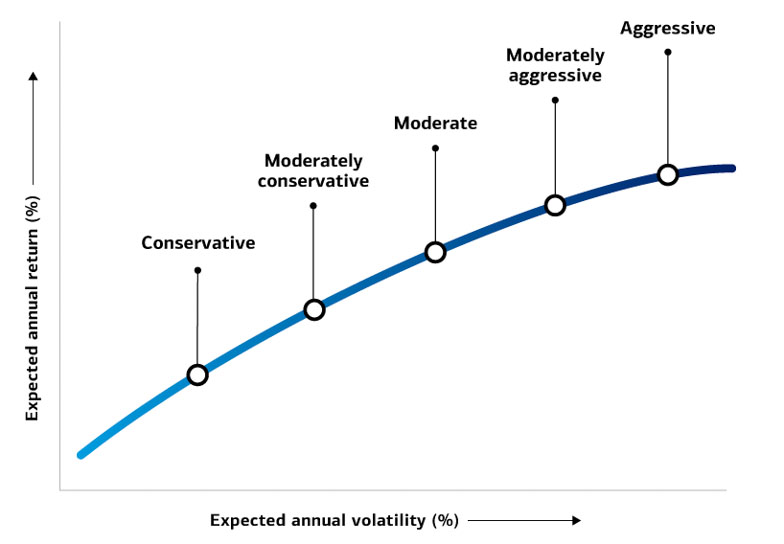

The tradeoff between risk and return

As you consider adjusting your investing style to pursue greater potential returns, ask yourself: “How comfortable will I be when the markets get volatile?”

Source: Chief Investment Office, “Foundations of Guidance,” December 2022. For illustrative purposes only.

Typically, the greater an investor’s risk appetite, the likelier they will be comfortable allocating a sizable portion of their portfolio to stocks and riskier fixed income investments such as high-yield bonds. While these investments have greater potential for loss, they also have the potential to deliver higher returns than more conservative, lower-risk investments such as high-quality corporate bonds, Treasurys and CDs.

Your financial ability to take risks

“Considering both your willingness and your financial ability to take on risk is the best way to make asset allocation choices that work for you.”

— portfolio construction and investment analytics executive, Chief Investment Office, Merrill and Bank of America Private Bank

Unlike your willingness to take risk, your ability to do so will shift, depending on your financial circumstances. While willingness is subjective, financial ability is based on an objective assessment of a number of factors, including:

Your liquidity, or cash, needs. Your ability to take on risk typically decreases as your need for cash for a specific goal approaches. The closer you are to needing the money, the less sense it makes to risk it by investing in stocks or bonds that could be at a low point when you sell them.

Your time horizon. On the other hand, when you have years until you need the money, your risk ability increases. With more time to ride out stock market ups and downs, you could withstand higher risks, such as a heavier investment in growth stocks or high-yield bonds to pursue potentially higher returns. With a shorter timeframe you don’t have that luxury.

The importance of the goal to your financial well-being. When the importance of the investment increases, your risk ability decreases. If you’re funding long-term care or saving for your children’s education, for instance, you may want to take a more moderate or even conservative approach to managing the assets allocated toward those goals so that you lower the risk of not being able to achieve them.

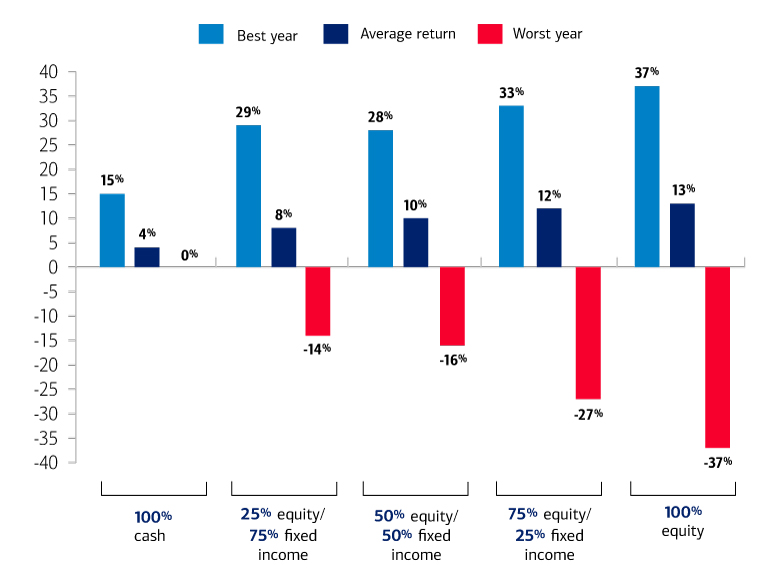

What kind of investor are you?

See how different investing approaches, from the most conservative (100% cash) to the most aggressive (100% equities), and degrees in between, have performed over time.

For illustrative purposes only. Notes: Historical returns are based on an analysis of actual investment returns from 1977 to 2022. Results shown are based on indexes and are illustrative; they assume reinvestment of income, no transaction costs or taxes, and the allocation remains constant over time. Past performance does not guarantee future results. Index sources: Stocks: S&P 500 Index; Bonds: ICE BofA U.S. Broad Market Bond Index; Cash ICE BofA 3-Month T-Bill Total Return Index. Direct investment cannot be made in an index. Diversification and asset allocation do not ensure a profit or protect against loss in declining markets. Source: Chief Investment Office. As of February 28, 2023.

How risk can help to shape your investment decisions

Understanding your willingness to take on risk can help you avoid making decisions that keep you up at night. Yet relying just on your subjective feelings could lead to investment choices that fail to meet your goals, says Suri. “Considering both your willingness and your financial ability to take on risk is the best way to make asset allocation choices that work for you,” he notes.

Say your goal is decades away. You’re conservative by nature and tempted to avoid volatile stocks and stick with low-risk bonds and cash. Yet those investments could leave you well short of what you need to retire on, especially when you factor in inflation. Ideally, to meet your goals, you should pursue investment strategies that have the potential to beat inflation. “Over the long term, stocks provide the highest rate of return,” Suri says, “and an investor whose goal is decades away should have plenty of time to recover from temporary market downturns.” A moderately aggressive portfolio containing mostly stocks, with bonds for diversification, could offer the peace of mind, as well as the growth, that this type of investor seeks.

Or, say you’re an aggressive investor with a stocks-only portfolio. “If you’re about to retire, or you’re saving for a down payment on a house in two years, your risk ability is much lower,” Vrdoljak cautions. “A sudden market downturn could sidetrack your financial goals.” A higher proportion of high-quality bonds and cash might make more sense.

Keep in mind that your ability for risk will change over time as your goals, cash needs and/or time horizons shift. So be sure to regularly review your asset allocation, risk willingness and financial ability for each of your goals, Vrdoljak suggests. “Taking a multi-factored approach to risk can make you feel more secure about the investment strategy you’re pursuing.”

1 Investor.gov, “Risk Tolerance.”

Diversification and asset allocation do not ensure a profit or protect against loss in declining markets.

Important Disclosures

Opinions are as of 06/15/23 and are subject to change.

Investing involves risk including possible loss of principal. Past performance is no guarantee of future results.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., (“Bank of America”) and Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S” or “Merrill”), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation (“BofA Corp.”).

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in foreign securities (including ADRs) involve special risks, including foreign currency risk and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are magnified for investments made in emerging markets. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration.

Risk management, diversification and due diligence processes seek to mitigate, but cannot eliminate risk, nor do they imply low risk.