Market briefs

Breaking insights on the economy, market volatility, policy changes and geopolitical events.

A brighter future for renewable energy stocks?

WITH RENEWABLE ENERGY EQUITIES TUMBLING by more than half since their highs in early 20211, investors may wonder if the sun has set on solar and wind. Yet, with another Earth Day upon us, the underlying drivers are as strong as ever, says Joe Quinlan, head of Market Strategy in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank. “We believe the global transition toward a clean energy future is still very much in progress.”

In the “Market Decode” video above, Quinlan looks at the myriad factors that drove clean energy stocks to new heights and more recently spurred their decline. He also highlights the forces shaping a potential comeback for the sector, as well as the market segments that could benefit from this ongoing shift in the global energy mix.

For a deeper dive, read “Renewable energy equities: What next after the boom and bust?” in this edition of the CIO’s Capital Market Outlook. You can find more on investing and the environment in “Climate risk and the markets: 5 key questions answered.” And be sure to check out our most recent Capital Market Outlook for the latest market news and insights.

EARTH DAY POP QUIZ: TEST YOUR KNOWLEDGE

Tap + to select correct answer and learn more

Q: True or false: The world’s biggest carbon dioxide emitter is also the world’s biggest renewable energy consumer?

How troubling are the interest costs on U.S. debt?

WITH FEDERAL INTEREST PAYMENTS REACHING $659 billion in 2023, some investors fear the government’s spiraling costs to service rising debts could disrupt the broader economy. “That’s a big, concerning number — nearly twice the level from 2020,” notes Joe Quinlan, head of Market Strategy for the Chief Investment Office (CIO) at Merrill and Bank of America Private Bank. “Fortunately, we believe the U.S. economy is large enough to limit any market impact.”

The situation. The spike reflects two dynamics, Quinlan notes in the latest CIO Capital Market Outlook report: A $9.5 trillion surge in U.S. debt from 2020 to 2023 and higher U.S. Treasury rates.

The concern: Higher government borrowing costs could push borrowing costs for businesses and individuals higher for longer, dragging the economy down in the short term.

Keeping perspective. Even at elevated rates, government interest payments represent about 2.4% of U.S. GDP.1 “That’s higher than over the past decade, but we see this as manageable for a $28 trillion economy that remains the most dynamic and innovative in the world,” says Quinlan.

Investment considerations. “Investors should follow the news but avoid precipitous reactions and instead stay well-diversified and focused on long-term investment goals,” Quinlan advises.

Tune in to the CIO’s Market Update audiocast series weekly to stay up to date on financial news that could affect your investments.

TEST YOUR MARKET KNOWLEDGE

Tap + to select correct answer and learn more

Q: What percentage of U.S. government spending goes to paying debt interest?

Investing in a year of election uncertainty

INVESTORS CONCERNED ABOUT THE POTENTIAL IMPACT of the 2024 U.S. election on the markets might take comfort in this history lesson, says Lauren J. Sanfilippo, senior investment strategist for the Chief Investment Office (CIO), Merrill and Bank of America Private Bank. “Heated election cycles are nothing new, and they’ve never slowed the world’s largest economy for long.” In fact, between 1945 and 2023, stocks on the S&P 500 have returned an annualized 11.4%1— with plenty of elections along the way, she notes.

Watch the “Market Decode” video above for specific ideas on how to help limit the potential effects of election-related volatility on your portfolio this year. For more in-depth insights, read “That Y2K feeling is back, but it’s political this time,” co-written by Sanfilippo, in the February 26 Capital Market Outlook and watch “Global elections and the markets: What to expect in 2024.”

Smart strategies to consider now for next year’s tax bill

AS YOU PULL TOGETHER YOUR 2023 TAXES, take some time to consider strategies that could help boost your savings and trim next year’s tax bill. From retirement to business taxes and more, opportunities available early in the year could be diminished if you wait until December, according to the National Wealth Strategies team in the Chief Investment Office (CIO). Here are three beginning-of-year tax strategies to consider:

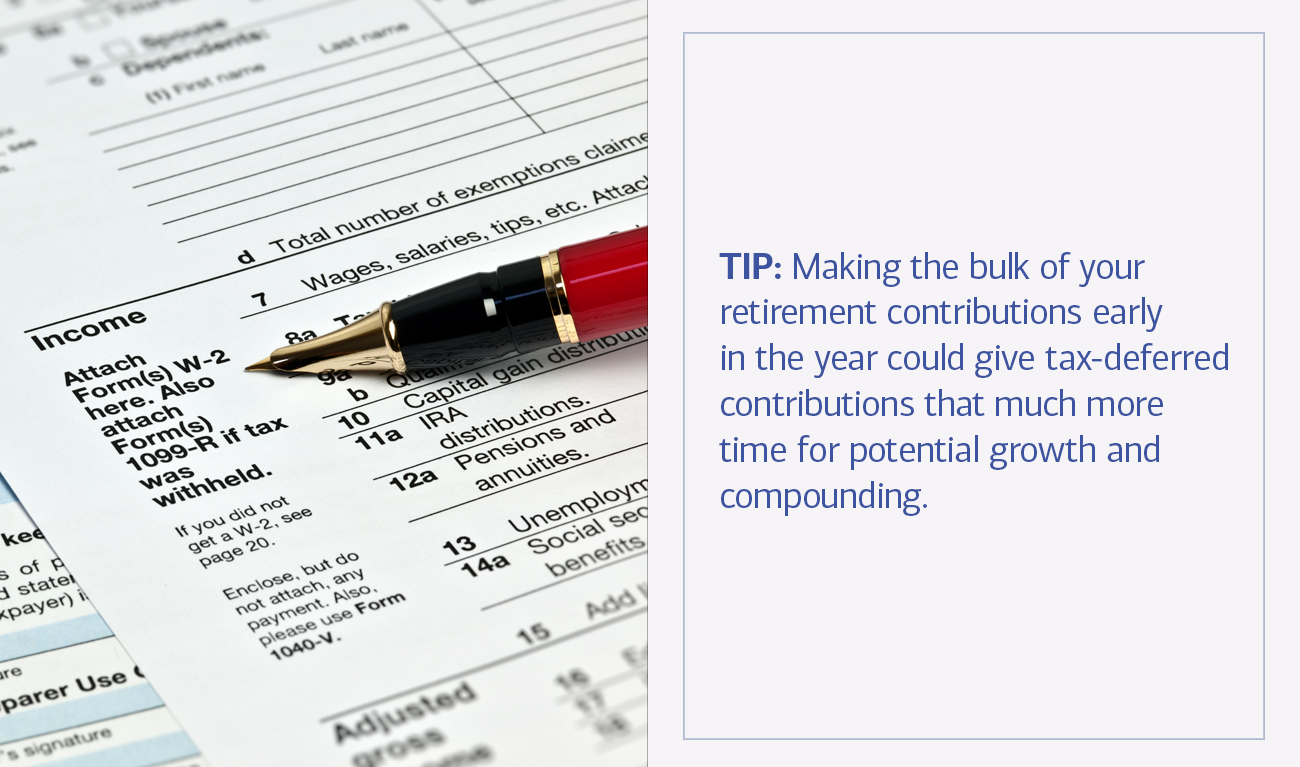

Front-loading your retirement plan contributions. You can make 2024 IRA contributions throughout the year — or even up to Tax Day in April 2025. But making the bulk of your contributions early in the year could give tax-deferred contributions that much more time for potential growth and compounding. The same holds if you contribute to a 401(k) plan. Just be aware that if you contribute early in the year and then stop in later months, your company’s 401(k) matching contribution, if offered, could also end or be delayed. Be sure to check your company’s matching policies.

March 15 deadline alert: Declare changes in your business status soon. If you’re converting your business from a C-corporation into an S-corporation this year, making the election by March 15 will enable you to be recognized under your new designation for federal tax purposes for all of 2024. If you miss that deadline, you’ll only be recognized for the portion of the year after you take the election (unless the IRS provides relief) — and that could have potentially significant tax consequences for your company.

Timing your RMDs carefully. The age at which people must begin taking required minimum distributions (RMDs) from tax-advantaged retirement accounts increased from 72 to 73 in 2023. If you turn 73 this year, you have until April 1, 2025 to take your first RMD. Granted, that move would allow you to defer taxes on any potential future growth. But waiting may not make sense for everyone. For instance, if you’re considering converting from a traditional to a Roth IRA — which doesn’t require RMDs — you’d have to take the RMD from your traditional IRA first, anyway.

In general, taking RMDs earlier rather than later can result in potential tax savings, because any future growth of the distributions, invested in a taxable account, would be taxed at the more favorable long-term capital gains rate. Your tax specialist can help you determine the best timing for your situation. Learn more about the ins and outs of RMD strategy by reading “Should you take your RMD earlier or later in the year?”

For a full rundown of year-ahead tax planning opportunities for 2024, including insights on inflation, charitable giving and stock options, read “Beginning of year tax planning” from the National Wealth Strategies team. And be sure to discuss any tax strategies with your tax professional and financial advisor.

What happened to that anticipated March rate cut?

EXPECTING THE FEDERAL RESERVE TO PIVOT from rate hikes to rate cuts, starting in March, investors rode a wave of anticipation, driving the DOW and S&P 500 indexes to new highs early in the year. Then came slightly higher than expected January Consumer Price Index (CPI) numbers (0.3 percent month over month, rather than an anticipated 0.2 percent increase.1), sending markets into a brief tizzy, with investors wondering: Should we be concerned about the economy?

Not to worry, says Matthew Diczok, Head of Fixed Income Strategy for the Chief Investment Office (CIO), Merrill and Bank of America Private Bank. Year over year, the latest CPI numbers showed a continuing downward trend — 3.1% from 3.4%.1 And though the Fed indicated that rate cuts were unlikely to happen in March, “We shouldn’t be alarmed if Fed officials appear to change their minds from month to month. What matters is the Fed’s overall mindset, and we believe they are firmly in easing mode for this year.”

Watch the video above to find out when the CIO believes the Fed will finally pivot, what it might mean for the markets and how you can prepare. And tune in to the CIO’s Market Update audiocast series for regular insights on the economy and the markets.

3 reasons to get off the sidelines and invest in equities

DESPITE PERIODIC VOLATILITY — as we saw after higher than anticipated January inflation numbers were released — the equity markets have performed exceptionally well so far this year. The S&P 5001 and the Dow Jones Industrial Average2 hit record highs, and the NASDAQ Composite Index has come close to its all-time high from 2021.3 While that’s good news for investors who already own stocks, those with significant cash on the sidelines may wonder if they’ve missed the boat. So, is getting into the market now too expensive?

That may be the wrong question to ask. “Valuation alone is not a good gauge of which way the market will trend,” says Emily Avioli, investment strategist in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank. One thing is certain: “Staying in cash because stocks seem too expensive — or the markets too volatile — could lead to potential missed opportunities,” she adds. Here’s why.

There’s room to grow. Markets are prone to periodic volatility related to inflation news, geopolitical concerns, presidential elections and more. “Yet we have seen 11 years with new all-time highs since the current secular bull market kicked off in 2013,” Avioli says. “And, given our view that it still has room to run, we could see years of new all-time highs ahead.”4

You can still find relative bargains. While S&P 500 stocks are trading at a price-to-earnings (P/E) valuation ratio of about 20.0x — well above the historical average of about 16x — “S&P 500 stocks outside of the mega-cap ‘Magnificent Seven’ companies have a current average P/E ratio of about 18x,” Avioli says. “And beyond the S&P 500, investors may find attractively priced small-cap and value stocks.”

“Consider using any near-term volatility as an opportunity to add to equities,” suggests Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank. “Corporate earnings remain healthy, and despite January’s higher than expected Consumer Price Index numbers, the CIO maintains its view that the Federal Reserve will likely begin a measured interest-rate cutting cycle in June or July.”

Cash carries its own risks. While it’s important to maintain some cash in your portfolio, cash typically hasn’t performed as well as stocks over the long term. In any given year, cash has a 24% chance of outperforming stocks, Avioli notes. But since 1979, over stretches of 15 or 20 years, stocks have outperformed cash.5

In the end, while it’s always preferable to pay less rather than more for a stock, valuation is just one factor to consider when you’re investing, Avioli adds. Other factors, including your long-term goals, risk tolerance and time horizon, are essential. “The best approach is to invest steadily in stocks, bonds and cash according to your long-term strategy.”

Learn more about investing in a bull market by reading “Considerations for investing at all-time highs” in the recent Capital Market Outlook from the CIO. And follow up by reviewing “How much is too much cash in your portfolio?”

1Reuters, “S&P 500 closes at record high; earnings, rate outlook in focus,” Feb. 7, 2024.

2 Morningstar, “Dow scores 12th record close ahead of U.S. inflation data,” Feb. 12, 2024.

3 Reuters, "Nasdaq slips from near all-time high, Dow up modestly ahead of inflation data,” Feb. 12, 2024.

4Bloomberg. Data as of February 7, 2024.

5 Bloomberg. Data as of January 31, 2024. The market is represented by the S&P 500 Index. Cash is represented by ICE BofA U.S. 3-month Treasury Bill Index. Refers to instances in which cash outperformed Equities over stated holding periods.

New goal: Limiting geopolitical risk in your portfolio

WHILE UKRAINE AND GAZA DOMINATE HEADLINES, they’re just two of more than 180 current regional conflicts, the highest number in 30 years.1 A global landscape marked by such rising tension and uncertainty could affect U.S. and global economies, markets — and investors — for years to come, notes Joe Quinlan, head of Market Strategy in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank.

“Don’t pause investing or diverge from your long-term strategy, but do consider geopolitics along with corporate earnings, valuations and other metrics when making investment decisions,” Quinlan suggests. Watch the “Market Decode” video above for tips on how to incorporate geopolitics into your investment decisions.

For more insights, read “Are the markets really impervious to geopolitical risks?” in the January 8, 2024 Capital Market Outlook, and tune in to the CIO’s Market Update audiocast series for weekly check-ins on the markets and economy.

1 International Institute for Strategic Studies, 2023. Bloomberg, “It’s Not Just Ukraine and Gaza: War is on the Rise Everywhere,” Dec. 10, 2023.

No one can predict the markets, but …

COMING OFF A YEAR WHEN THE S&P 500 rose by 26%,1 inching toward a new record, many investors want to know: Will the markets maintain their momentum in 2024? “Trying to predict the markets is never wise — and that’s particularly true in such an unpredictable investment landscape,” says Joe Quinlan, head of Market Strategy for the Chief Investment Office (CIO) at Merrill and Bank of America Private Bank. But some compelling clues do exist.

A recent Capital Market Outlook report, “10 macro questions for 2024,” written by Quinlan and Lauren Sanfilippo, senior investment strategist for the CIO, features informed insights (and a few qualified predictions) as they answer 10 questions that may be top of mind for you. Here’s a sampling — read the full report for their thoughts on whether all the good news is already priced into the stock market, how close the Fed is to beating inflation, and more.

Will the 2024 U.S. election create volatility — or opportunity?

“Asset prices are determined more by economic fundamentals than by politics,” notes Sanfilippo. “Presidential elections do create market uncertainty, but disruptions are usually temporary.” Volatility will likely depend on what stances the parties take on taxes, immigration, healthcare and other issues, she adds. It’s worth noting, too, that the U.S. isn’t the only country holding a major, potentially consequentical election this year.

What it could mean for investors: “Temporary election volatility may allow long-term investors to strategically add to portfolios at attractive prices,” Sanfilippo says.

What’s the likely impact of geopolitical unrest?

“Amid wars in Europe and the Middle East, shipping lane disruptions, U.S.-China tensions and cybersecurity threats, geopolitical unrest has become a significant variable for investors,” says Quinlan. While these tensions represent one of this year’s major market risks, “quicker-than-expected resolutions to the major global conflicts could be among several potential surprises contributing to market growth this year,” he adds.

What it could mean for investors: The fluid global landscape favors high-quality diversified assets with an emphasis on energy and copper, large defense companies and cyber leaders.

How could artificial intelligence (AI) move markets in 2024?

“AI innovations have been building since late 2022, and companies across industries and sectors have ratcheted up their capital spending,” Sanfilippo says. “While the magnitude and timing of AI’s effect on corporate earnings will vary, in 2024 we should see AI applications spreading to non-tech industries.”

What it could mean for investors: Sectors such as education, healthcare and manufacturing should benefit. But the growing push for regulation of AI could affect its impact on earnings and productivity.

While there’s plenty of room for positivity about the markets and economy, “we remain optimistic — but realistic — about where asset price returns can be in 2024,” concludes Quinlan. For more on the year ahead, watch “Looking toward a new era of growth.”

TEST YOUR MARKET KNOWLEDGE

Tap + to select correct answer and learn more

Q: How much is currently sitting on the sidelines in money market funds, ready for investors to deploy?

1 Bloomberg. Data as of December 2023.

Getting comfortable with “higher for longer”

HFL STANDS FOR “HIGHER FOR LONGER,” and it doesn’t just apply to interest rates anymore, says Joe Quinlan, head of CIO Market Strategy. Given the tight labor market, strong wages and elevated energy prices, it’s unlikely rate cuts will come any time soon, Quinlan explains. Markets and investors have pretty much accepted that fact. But the HFL trend also applies to a number of other areas that could affect the markets and your investing decisions. Among them: global energy prices, defense spending and the U.S. deficit.

Watch the video above for what these higher-for-longer trends could mean for your portfolio. For more insights, read “Higher-for-Longer Goes Beyond Interest Rates: What Investors Need to Know” in the October 10, 2023 Capital Market Outlook and tune in to the CIO’s Market Update audiocast series for weekly insights on the markets and economy.

Important Disclosures

Investing involves risk, including the possible loss of principal. Past performance is no guarantee of future results.

Opinions are as of the date of these articles and are subject to change.

Bank of America, Merrill, their affiliates, and advisors do not provide legal, tax, or accounting advice. Clients should consult their legal and/or tax advisors before making any financial decisions.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., (“Bank of America") and Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S" or “Merrill"), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation (“BofA Corp.”).

All recommendations must be considered in the context of an individual investor’s goals, time horizon, liquidity needs and risk tolerance. Not all recommendations will be in the best interest of all investors.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors.

These risks are magnified for investments made in emerging markets. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors.

Income from investing in municipal bonds is generally exempt from Federal and state taxes for residents of the issuing state. While the interest income is tax-exempt, any capital gains distributed are taxable to the investor. Income for some investors may be subject to the Federal Alternative Minimum Tax (AMT).

Retirement and Personal Wealth Solutions is the institutional retirement business of Bank of America Corporation (“BofA Corp.”) operating under the name “Bank of America.” Investment advisory and brokerage services are provided by wholly owned non-bank affiliates of BofA Corp., including Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as "MLPF&S" or "Merrill"), a dually registered broker-dealer and investment adviser and Member SIPC. Banking activities may be performed by wholly owned banking affiliates of BofA Corp., including Bank of America, N.A., Member FDIC.

You have choices about what to do with your 401(k) or other type of plan-sponsored accounts. Depending on your financial circumstances, needs and goals, you may choose to roll over to an IRA or convert to a Roth IRA, roll over a 401(k) from a prior employer to a 401(k) at your new employer, take a distribution, or leave the account where it is. Each choice may off er different investments and services, fees and expenses, withdrawal options, required minimum distributions, tax treatment (particularly with reference to employer stock), and provide different protection from creditors and legal judgments. These are complex choices and should be considered with care.

Diversification does not ensure a profit or protect against loss in declining markets.

Sustainable and Impact Investing and/or Environmental, Social and Governance (ESG) managers may take into consideration factors beyond traditional financial information to select securities, which could result in relative investment performance deviating from other strategies or broad market benchmarks, depending on whether such sectors or investments are in or out of favor in the market. Further, ESG strategies may rely on certain values based criteria to eliminate exposures found in similar strategies or broad market benchmarks, which could also result in relative investment performance deviating.